Bitcoin

The rise of Bitcoin ETFs and future market implications

The following is a guest post by Shane Neagle.

Regardless of an asset’s fundamentals, its value is governed by an underlying characteristic – market liquidity. Is it easy for the general public to sell or buy this asset?

If the answer is yes, then the asset receives a high trading volume. When this happens, it is easier to execute trades at varying price levels. In turn, a feedback loop is created – more robust price discovery increases investor confidence, which encourages greater market participation.

Since Bitcoin’s launch in 2009, it has relied on cryptocurrency exchanges to establish and expand its market depth. The easier it became to trade Bitcoin across the world, the easier it was for the price of BTC to rise.

Likewise, when fiat-to-crypto rails like Mt. Gox or FTX fail, the price of BTC suffers greatly. These are just a few obstacles in the way of Bitcoin legitimization and adoption.

Bitcoin’s journey to mainstream finance. Image credit: Pantera Capital

However, when the Securities and Exchange Commission (SEC) approved 11 spot-traded Bitcoin exchange-traded funds (ETFs) in January 2024, Bitcoin gained a new layer of liquidity.

This is a liquidity milestone and a new layer of credibility for Bitcoin. Entering the world of regulated exchanges, alongside stocks, exhausted the naysayers who questioned Bitcoin’s status as a decentralized digital gold.

But how will this new market dynamic play out over the long term?

The democratization of Bitcoin through ETFs

From the beginning, The new thing about Bitcoin has been its weakness and strength. On the one hand, it is a monetary revolution to hold wealth in your head and then be able to transfer that wealth without borders.

Bitcoin miners can transfer it without permission and anyone with internet access can become a miner. No other asset has this property. Even gold, with its relatively limited supply and resistance to inflation, can easily be confiscated, as happened in 1933 under Executive Order 6102.

This means that Bitcoin is an inherently democratizing vehicle of wealth. But with self-custody comes great responsibility and room for error. Glassnode data shows that around 2.5 million bitcoins have become inaccessible due to the loss of seed words that can regenerate access to the Bitcoin mainnet.

This represents 13.2% of Bitcoin’s fixed supply of 21 million BTC. Indeed, self-custody induces anxiety among both retail and institutional investors. Would fund managers engage in Bitcoin allocation with such risk?

But Bitcoin ETFs have completely changed this dynamic. Investors looking to protect themselves against currency devaluation can now delegate custody to large investment firms. And they, from BlackRock and Fidelity to VanEck, delegate it to chosen cryptocurrency exchanges like Coinbase.

Although this reduces Bitcoin’s self-custody feature, it increases investor confidence. At the same time, miners, through proof of work, still make Bitcoin a decentralized asset regardless of how much BTC is accumulated in ETFs. And Bitcoin remains a digital asset and a solid asset based on computing power (hashrate) and energy.

Bitcoin ETFs reshaping market dynamics and investor confidence

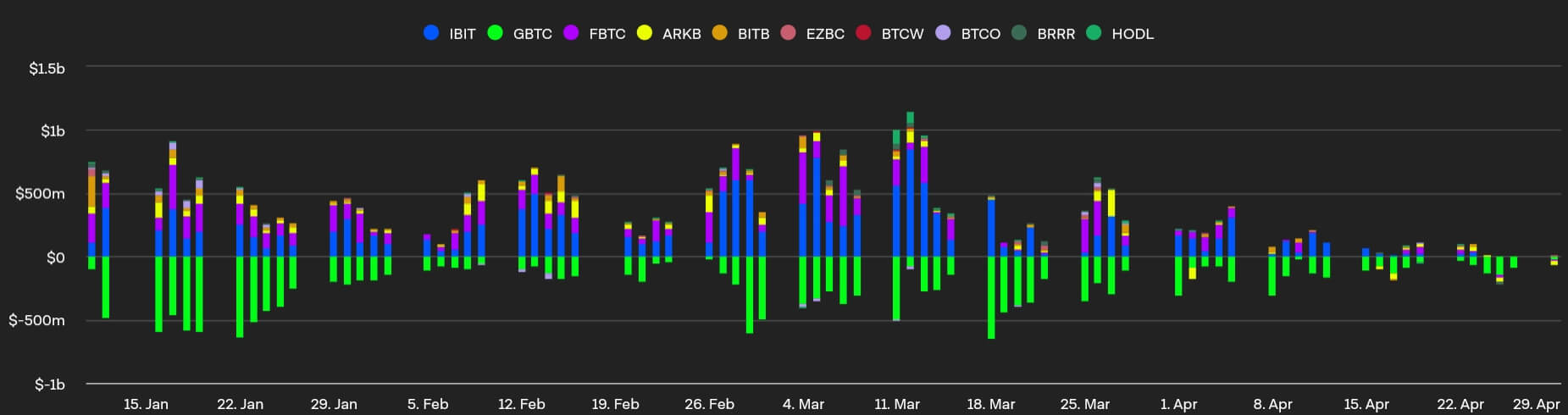

Since January 11, Bitcoin ETFs have opened the floodgates of capital to deepen the depth of the Bitcoin market, resulting in a cumulative volume of $240 billion. This substantial inflow of capital has also changed the equilibrium price for many investors, influencing their strategies and expectations about future profitability.

However, despite the launch being largely successful in exceeding expectations, negative outflows gained ground as the Bitcoin ETF hype subsided.

On April 30, Bitcoin ETF inflows yielded negative $162 million, marking the fifth consecutive day of negative outflows. For the first time, Ark’s ARKB outflow (yellow) surpassed GBTC (green), at negative $31 million versus $25 million, respectively.

Considering this occurred after the 4th Bitcoin halving, which reduced Bitcoin’s inflation rate to 0.85%, it is safe to say that macroeconomic and geopolitical concerns temporarily overshadowed Bitcoin’s fundamentals and deepened the market’s depth.

This became even more evident when the opening of Bitcoin ETFs by the Hong Kong Stock Exchange did not work. Despite opening access to capital to Hong Kong investors, the volume represented just US$11 million ($2.5 million in Ether ETFs), compared to the expected US$100 million.

In short, the crypto ETF debut in Hong Kong was almost 60 times smaller than in the US. Although Chinese citizens with companies registered in HK can participate, investors from mainland China are still prohibited.

Likewise, given that the New York Stock Exchange (NYSE) is approximately five times larger than the HKSE, the HKSE’s Bitcoin/Ether ETFs are not likely to exceed $1 billion in flows in the first two years. , according to ETF analyst Bloomberg. Eric Balchunas.

Future Perspectives and Potential Challenges

During the Bitcoin ETF liquidity extravaganza, BTC price tested the limit above $70K several times, reaching a new all-time high of $73.7K in mid-March.

However, miners and holders took advantage of the opportunity to exert selling pressure and reap gains. With sentiment now down to the $60,000 range, investors will have greater opportunities to buy Bitcoin at a discount.

Not only is Bitcoin’s inflation rate at 0.85% after the fourth halving, versus the Fed’s dollar target of 2%, but more than 93% of the BTC supply has already been mined. The flow of BTC mined went from ~900 BTC daily to ~450 BTC daily.

This translates into greater scarcity of Bitcoin, and what is scarce tends to become more valuable, especially after legitimizing Bitcoin investment on an institutional level through Bitcoin ETFs. So much so that Bybit’s analysis predicts supply shock on exchanges by the end of 2024. Alex Greene, senior analyst at Blockchain Insights, said:

“The increase in institutional interest has stabilized and drastically increased demand for Bitcoin. This increase will likely worsen shortages and increase prices after the halving.”

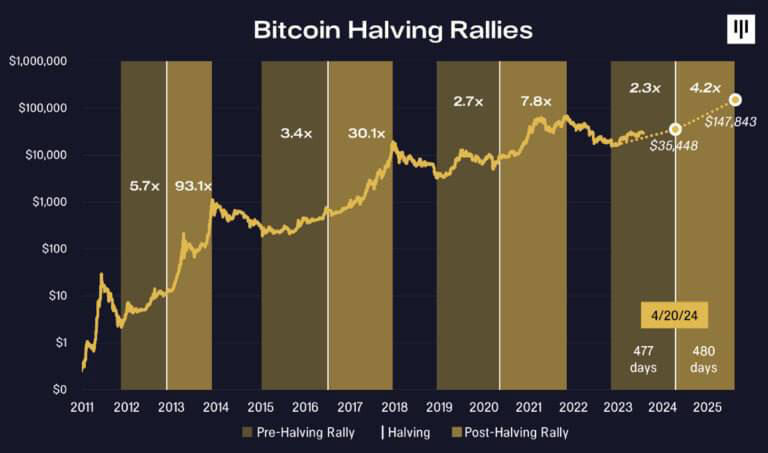

After previous halvings in the absence of the Bitcoin ETF environment, Bitcoin price rose to 7.8x gains in 480 days. While a higher Bitcoin market cap makes these gains less likely, multiple valuation increases remain in play.

However, market volatility is still expected in the meantime. With Binance situation resolvedIn addition to leaving behind the series of crypto bankruptcies during 2021, the main source of FUD remains the government.

Despite Tom Emmer’s efforts, as the majority of the Republican Party argues, even self-custody wallets could be targeted as money transmitters. The FBI suggested this direction recently with the Notice against the use of “unregistered cryptographic money transmission services”.

Likewise, this year, the Federal Reserve’s guidance on interest rates could suppress appetite for risky assets like Bitcoin. However, the perception of Bitcoin and the market surrounding it has never been so mature and stable.

If the regulatory regime changes course, small businesses may even abandon solutions like invoice financing and switch to a BTC ETF supported system.

Conclusion

After years of Bitcoin ETF rejections for spot trading, these investment vehicles have erected new liquidity bridges. Even suppressed by Barry Silbert’s gray scale (GBTC), they revealed a large institutional demand for an appreciating commodity.

With the fourth Bitcoin halving, increasing scarcity and fund managers’ allocations are now a certainty. Furthermore, the prevailing sentiment is that fiat currencies will be perpetually devalued as long as a central bank exists.

After all, how could governments continue to finance themselves despite gigantic budget deficits?

This makes Bitcoin even more attractive in the long term after holders reap the profits from the new ATH points. Between these peaks and troughs, Bitcoin’s bottom will likely continue to rise in the deeper institutional waters.